- Credit standards remained broadly unchanged for both loans to enterprises and housing loans

- Demand for loans to enterprises declined, while demand for housing loans increased further

- Euro area banks use TLTRO-III liquidity largely for granting loans

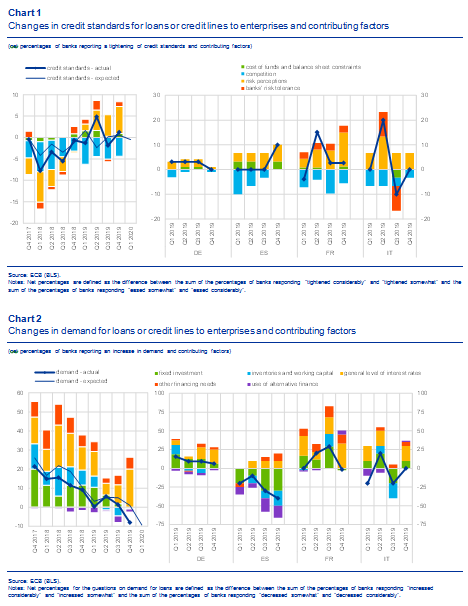

Credit standards – i.e. banks’ internal guidelines or loan approval criteria – remained broadly unchanged for both loans to enterprises and loans to households for house purchase in the fourth quarter of 2019, according to the January 2020 bank lending survey (BLS), in line with expectations expressed in the previous survey round. Credit standards for consumer credit and other lending to householdstightened further, despite expectations that they would remain broadly unchanged. Risk perceptions (relating to both the general economic situation and the firm-specific situation) continued to have a tightening impact on the credit standards applied to loans to enterprises. Looking ahead to the first quarter of 2020, banks expect credit standards for loans to enterprises to remain unchanged, while they expect credit standards to tighten for housing loans and to ease for consumer credit and other credit to households.

Banks’ overall terms and conditions – i.e. the actual terms and conditions agreed in loan contracts –remained broadly unchanged in the fourth quarter of 2019 for new loans to enterprises and housing loans, while they eased for consumer credit.

Net demand for loans to enterprises declined in the fourth quarter of 2019 (the first time this had been seen since the fourth quarter of 2013), despite banks expecting it to remain stable overall. That decline in net demand was broadly based across a number of larger and smaller euro area countries. Demand for loans to enterprises continued to be supported by the low general level of interest rates and, to a lesser extent, M&A activities. In contrast, financing needs for fixed investment ceased to contribute positively to firms’ loan demand. Net demand for housing loans increased further in the fourth quarter of 2019, driven mainly by the low general level of interest rates, while favourable housing market prospects and consumer confidence also contributed positively. The use of alternative sources of finance continued to have a slightly negative effect on demand. Meanwhile, net demand for consumer credit and other lending to households increased in the fourth quarter of 2019, driven by the low general level of interest rates, consumer confidence and increased spending on durable goods.

Euro area banks reported that regulatory or supervisory action continued to have a strengthening impact on their capital positions in the second half of 2019, as well as a tightening impact on credit standards across all loan categories (with further tightening expected over the next six months).

Respondent banks also reported that non-performing loans (NPLs) had a small tightening impact on credit standards for loans to enterprises and consumer credit in the second half of 2019 (and a broadly neutral impact on credit standards for housing loans). Risk perceptions and risk aversion were the main drivers of the tightening impact of NPL ratios.

As regards the impact of the third series of targeted longer-term refinancing operations (TLTRO-III), euro area banks reported that they used TLTRO-III liquidity largely for the purpose of granting loans to the non-financial private sector. Given the attractive conditions surrounding TLTRO-III operations, the profitability motive has been the most important reason for banks to participate so far. As regards their lending policies, banks reported that TLTRO-III operations had a net easing impact on their terms and conditions in the second half of 2019, with a smaller easing impact on credit standards and a positive net impact on lending volumes.

The euro area bank lending survey, which is conducted four times a year, was developed by the Eurosystem in order to improve its understanding of banks’ lending behaviour in the euro area. The results reported in the January 2020 survey relate to changes observed in the fourth quarter of 2019 and expected changes in the first quarter of 2020, unless otherwise indicated. The January 2020 survey round was conducted between 6 and 27 December 2019. A total of 144 banks were surveyed in this round, with a response rate of 100%.

Notes

- A report on this survey round is available at https://www.ecb.europa.eu/stats/ecb_surveys/bank_lending_survey/html/index.en.html. A copy of the questionnaire, a glossary of BLS terms and a BLS user guide with information on the BLS series keys can also be found on that web page.

- The euro area and national data series are available on the ECB’s website via the Statistical Data Warehouse (http://sdw.ecb.europa.eu/browse.do?node=9691151). National results, as published by the respective national central banks, can be obtained via https://www.ecb.europa.eu/stats/ecb_surveys/bank_lending_survey/html/index.en.html.

- For more detailed information on the bank lending survey, see Köhler-Ulbrich, P., Hempell, H. and Scopel, S., “The euro area bank lending survey”, Occasional Paper Series, No 179, ECB, 2016 (http://www.ecb.europa.eu/pub/pdf/scpops/ecbop179.en.pdf).

www.ecb.europa.eu

pixabay.com